》Check SMM copper quotes, data, and market analysis

》Subscribe to view historical spot metal prices from SMM

》Click to access the SMM copper industry chain database

>Macro side, during the Labour Day holiday, US stocks rebounded, and European and Asian stock indices warmed up, with short-term corrections in market expectations for US Fed interest rate cuts. The April US non-farm payrolls data outperformed expectations, while the unemployment rate did not rise significantly, indicating moderate resilience in the US economy. However, the Q1 GDP decline of 0.3% YoY exposed weak domestic demand, with structural factors showing intensified "import rush" behavior by US enterprises, adding inventory pressure. The market implied two major imbalances: first, the conflict between expectations for US Fed interest rate cuts and fiscal deficit expansion, which could push up long-term US Treasury yields; second, the challenge posed to the US financial system's solvency by weakened US dollar liquidity in Asian and European markets. Due to OPEC+ production increases, international oil prices plummeted during the Labour Day holiday. Meanwhile, as Sino-US trade tensions eased, the offshore RMB appreciated sharply against the US dollar, recovering the losses incurred after the implementation of reciprocal tariffs in April. The non-ferrous metals sector gradually warmed up after a sharp decline on May 1, with LME copper hitting a low of $9,088/mt during the holiday and strengthening back above $9,300/mt.

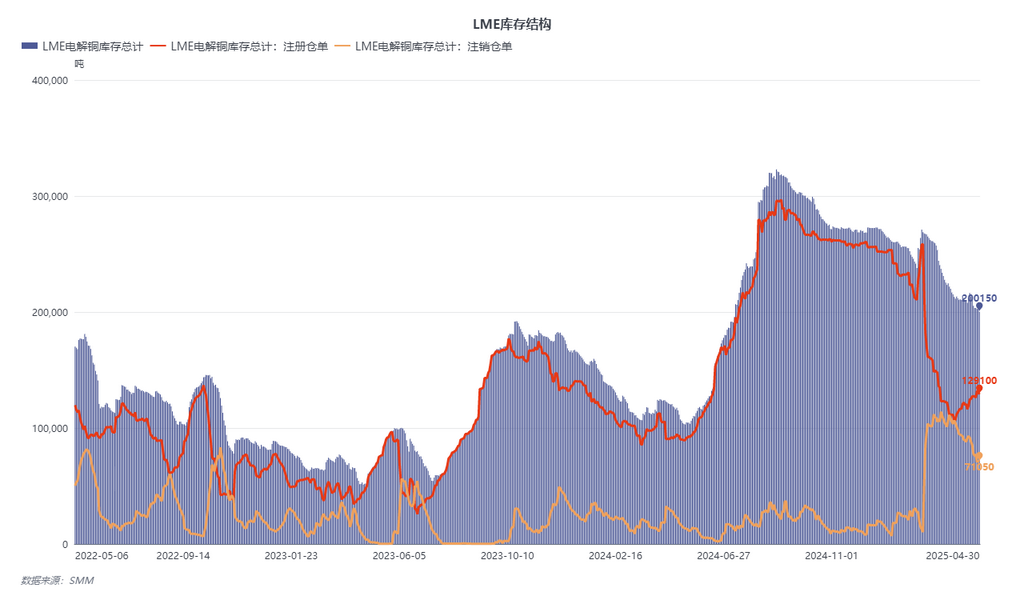

>Fundamentals side, during the Labour Day holiday, LME inventories continued to destock. Although the ratio of cancelled warrants declined compared to the previous period, it remained at historically high levels. Meanwhile, the liquidity of registered warrants significantly decreased: currently, around 65,000 mt of Russian copper cathode is held in registered warrants, with only about 60,000 mt of registered copper cathode inventory remaining in Asia. On April 30, LME received approximately 20,000 mt of warrant cargo pick-up applications, mostly from large overseas traders. The current global copper cathode apparent inventory structure has significantly reversed compared to the same period in 2024, with the market on alert for potential high backwardation structures and supply deficits.

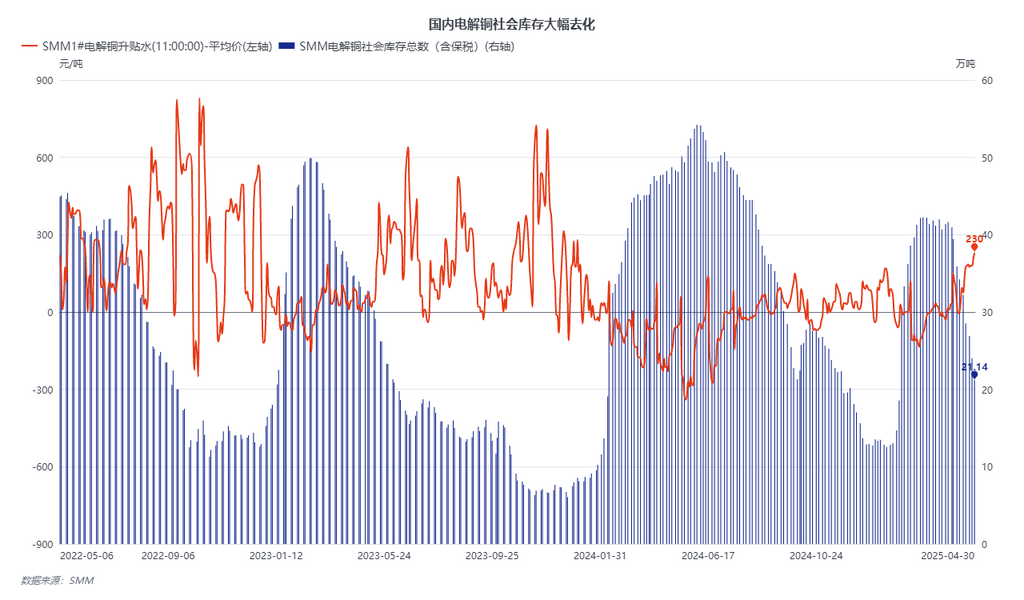

>Domestically, according to SMM, China's copper cathode production in April still increased compared to expectations. SMM's China copper cathode production in April was 1.1257 million mt, up 3,600 mt MoM, a 0.32% increase, and up 14.27% YoY. The cumulative production from January to April was 4.3198 million mt, up 415,100 mt YoY, a 10.63% increase. Meanwhile, domestic social inventories destocked by nearly 200,000 mt in April. Based on monthly imports of 300,000 mt, China's actual copper cathode consumption in April approached 1.5 million mt, expected to hit a record high. Due to significant destocking, the SHFE structure also significantly reversed compared to the same period in 2024, with SHFE calendar spreads shifting towards longer-dated positions. Downstream enterprises remained vigilant against potential extreme backwardation structures, overstocking inventories during the holiday. Thus, overall apparent consumption improved.

>Looking ahead, the global copper concentrate tightness remains unchanged. Affected by tariff policies, US copper concentrates originally destined for China have been redirected to regions such as Japan, South Korea, and India. Meanwhile, unexpected disruptions in overseas supply chains have occurred. As the Altonorte smelter in Chile has yet to resume production, South American copper cathode port arrivals are expected to decline in May-June. Additionally, copper cathode exports from the DRC face obstacles, with CIF port arrivals in May expected to remain tight. Large traders in the market hoarding unreported inventory may accelerate the rise in domestic and overseas copper cathode premiums. Due to the continuous pullback in crude oil prices, the market expects sulphuric acid prices to fall correspondingly in Q2. The key benefit that supported smelter production profits in Q1 has weakened, and overseas smelters may face extended maintenance or passive production cuts in Q2 due to this impact. Overall, supply disruptions in copper fundamentals are significant, with the possibility of extreme structures emerging in May greatly increasing.

>

![Physical premiums dropped significantly, while forward buying interest emerged [SMM Yangshan spot copper]](https://imgqn.smm.cn/usercenter/ZroQZ20251217171712.jpg)